CS3 CIMA Strategic Case Study Exam 2021 Free Practice Exam Questions (2026 Updated)

Prepare effectively for your CIMA CS3 Strategic Case Study Exam 2021 certification with our extensive collection of free, high-quality practice questions. Each question is designed to mirror the actual exam format and objectives, complete with comprehensive answers and detailed explanations. Our materials are regularly updated for 2026, ensuring you have the most current resources to build confidence and succeed on your first attempt.

A month has passed since you submitted the report requested by William Seaton, Director of Finance on the Board’s proposals.

You have received the following email:

From: William Seaton, Director of Finance

To: Finance Manager

Subject: Shale oil

Hi,

One of the geologists made a presentation to the Board, proposing that we investigate the extraction of shale oil deposits. I have attached the slides that were used as the basis for this presentation.

I need you to work on a response to this document:

Firstly, what risks do you envisage in our entry to the shale oil business?

Secondly, what do you regard as the key factors that we should consider when deciding on proceeding with this

proposal? Please justify your selection.

Thirdly, what factors should we take into account when deciding on which country or countries to commence this

side of the business?

Finally, what are the challenges in creating a team of technical staff to lead our efforts in this area?

William

The presentation slides can be found by clicking on the Reference Materials button.

You received a telephone call at home early in the morning, asking you to check your emails. The following email was waiting for you:

From: William Seaton, Director of Finance

To: Finance Manager

Subject: Public relations crisis

Hi,

This email arrived from the Head of our Middle East office just now. They are a few hours ahead of us, so he rang me at home to make sure that I had seen his message.

We have a few hours before the news article will be published, so I need to make the best use of that time in order to limit the damage to Slide. Your priority is to protect our reputation because I have already woken up the engineers and geologists and they are going to deal with the actual oil spillage.

I am not thinking too clearly, so I need you to provide some initial thoughts on the following:

Should we use our business relationship with Business News to have them withdraw the story? We are a major advertiser and we spend millions with them every month. What are the advantages and disadvantages?

Should we respond with the facts as we know them? All we know for certain is that there have been reports of oil contamination in an area that has countless oil facilities nearby, and so we could deny all responsibility, at least until our experts have had the chance to get there and to investigate.

If we do decide to make a public announcement then we will need to have a plan in place. We need to assemble a team to deal with the press. How should we structure our media response team?

What are the key factors that the Board should consider when communicating with the press? Explain why the factors that you have identified are important.

I realise that it is still very early, but I need your thoughts very quickly.

Thanks

William

The email referred to above can be found by clicking on the Reference Materials button.

Memorandum of Understanding between Fouce Oil and Slide

It is proposed that Fouce Oil and Slide will temporarily combine their exploration activities, with Slide taking overall control in recognition of the greater expertise of its professional exploration staff.

This collaboration will work as follows:

1.Slide will take responsibility for the management and operation of all future exploration activities for the two companies, with effect from 1 October 2015.

2.Fouce Oil will second all of its professional oil exploration staff to Slide. Fouce will continue to employ these staff and will pay their salaries.

3.Slide will brief Fouce Oil’s professional oil exploration staff on all operational matters relating to exploration activities for the duration of this arrangement.

4.The provisions of paragraph 3 will apply to any projects in which Slide participates with third parties on a farm-in or other joint venture basis.

5.In recognition of Slide’s greater expertise, Fouce Oil will offer its entire portfolio of existing exploration rights to this venture, without any charge to Slide. Fouce Oil will also pay for 55% of any and all exploration costs, leaving Slide responsible for the remaining 45%.

6.The revenues from all successful discoveries will be shared equally by Slide and Fouce Oil. In the event that either party wishes to sell an oil well, the other will have the option of purchasing the other’s rights for 50% of the well’s agreed valuation.

7.This arrangement will be subject to review at the end of five years and annually thereafter. In the event that either party wishes to discontinue the arrangement, all ongoing exploration projects will be drawn to an orderly conclusion.

Signed

Thomas Yip, Chief Executive Officer, Fouce Oil

Andrew Jones, Chief Executive Officer, Slide

14 May 2015

The following email has been forwarded to you by William Seaton, Director of Finance:

From: William Seaton, Director of Finance

To: Finance Manager

Subject: Yesterday’s Board meeting

Hi,

One of my fellow Board members made a brief presentation to the Board. I am attaching the slides that were used in this presentation.

I have to say that I thought that some of the advice being offered to the Board was incorrect, but I would rather make a positive contribution to the discussion and so I said very little.

I need you to email me your thoughts on the following:

Your views on the presentation relating to tax matters

Your views on the briefing relating to the decision making process

Your views on the briefing’s recommendations on driving performance

Finally, an alternative briefing note on driving performance. Ideally, that should be two or three headings, with a

clear explanation for each.

As usual, this is urgent. Many thanks for your help so far with this project.

William

The slides can be found by clicking on the Reference Materials button.

The Director of Finance, William Seaton, has stopped you in the corridor:

“Your report was really helpful, but the Board is still considering the implications of that email from Jan Archibald at Fouce Oil. I need to make a more detailed report to the Board and I would like you to draft it for me.

I know that we have owned and operated oil wells in the past, but that has always been with the intention of finding a buyer who is prepared to pay a realistic price. We have chosen never to think about the implications of keeping wells.

I need a report from you that covers the following issues:

The key political risks of retaining our interest in these oil wells, with particular emphasis on high consequence, high likelihood risks.

A suitable response to each of your political risks.

An overview of how changes in the global economy and the demand for oil could affect the decision to proceed.

The challenges associated with putting together a management team to take charge of the production side of this proposed new

strategy.

I realise that this is a lot to ask of you, but I need you to move quickly because of the interest from our biggest shareholder.”

Two months have passed since the threatened disruption of the building work on the biomass power station. The threat has been resolved and work is again under way on the development.

You have received the following email from Peter Sorchi, CEO:

From: Peter Sorchi, Chief Executive Officer

To: Senior Finance Manager

Subject: Wildlife survey

Hi,

I tried to obtain some trustworthy advice from your boss this afternoon, but have come away feeling quite unsure that we are on the same wavelength.

As you know, the law in Marland is very clear concerning the protection of rare species of wildlife. Before building work commences on our new power station the Government will send a survey team to check for the presence of protected species. The attached article shows how sensitive an issue this can be.

As part of our corporate social responsibility, every one of Wodd’s forestry teams has a small team of wildlife officers, whose job is to survey the forest and to identify all natural habitats. Trees can grow undisturbed for many years in a commercial forest before they are harvested and so natural habitats can become well established. Our wildlife surveys enable us to limit the harm done when trees are felled.

One of Wodd’s wildlife officers in the North Forest has submitted a report on the sighting of a rare species of bat in the area that will be cleared for the power station. The report states that these creatures tend to be difficult to observe because they only come out very late at night and tend to roost in dense forest. This could, potentially, delay the start of work for six months while the bats are captured and relocated. Relocating the bats will also be expensive.

The Finance Director’s advice was to ask the wildlife officer to change the report, stating that the original version was submitted in error and that the sighting occurred in a completely different part of the forest, well away from the planned construction site. There is only a small possibility that the Government inspectors will find the bats during their own inspection. In the event that they do then Wodd can claim that it was unaware of the bats’ presence.

This whole exchange raises a number of issues for me.

Should we spend shareholder money on protecting wildlife in our forests?

What are the implications for our internal control system of the Finance Director asking for this report to be changed?

What are the difficulties in motivating our wildlife officers and how might we overcome these?

The Chairman is always complaining about how the executive directors are too aggressive when it comes to making a profit. How might I address that concern?

I would appreciate your response on each of the above issues.

Peter

The formal merger with Darrell has been negotiated and the legal formalities have been completed. The two company management teams are working on the integration of the two businesses.

You receive an email from Peter Sorchi, the Chief Executive of the merged company:

From: Peter Sorchi, Chief Executive Officer

To: Senior Finance Manager

Subject: Integration of IT and treasury

Hi,

I need you to advise me on a couple of matters. The attached press clipping shows how sensitive this is.

We need to integrate the IT and treasury functions of the former Wodd and Darrell. I thought that it would be a simple matter of identifying the common ground and slimming down both companies’ departments to cover the new entity, but I have the heads of both IT and treasury from each company arguing that their approaches are better for the merged group and that they should take the lead.

Wodd’s Treasurer claims to be an expert in natural hedging of currency risks and Darrell’s argues that her department was highly successful because it makes excellent use of derivatives for hedging. Both agree only on the fact that they cannot work together. I am afraid that I have to agree with them on that and the Board will have the difficult decision of choosing between them.

I have the opposite problem with the IT function. The two Heads of IT are excited to be able to combine their databases and to develop their respective interests in Big Data. They claim that we should retain all of the professional staff in both departments and possibly even expand the merged IT Department beyond that. Given the rationalisation in all of our other functions, I do not think that we can agree to that, but I would hate to throw away a worthwhile opportunity.

Please give me your thoughts on the following:

What approach to hedging is more likely to meet our needs: natural hedging or heavy use of derivatives?

Ignoring hedging, what other factors should we consider in deciding between the two treasurers?

Are the two heads of IT likely to be correct in arguing that we need to retain all existing IT staff in order to exploit synergies in data, particularly opportunities to leverage Big Data?

What would the challenges be in motivating them to reduce their joint staffing levels and how might we deal with these?

Peter

Two weeks have passed since the article about Wodd’s role in tax avoidance was published. Thankfully, the initial reaction was to condemn the celebrities who invest in tax avoidance and little was said about Wodd’s role in facilitating tax-efficient investments.

You have received the following email from Sarah Johns, Marketing Director:

From: Sarah Johns, Marketing Director

To: Senior Finance Manager

Subject: Forestry certification

Hi,

I am told that you would be a good person to talk to concerning the practical implications of a new venture that has been proposed.

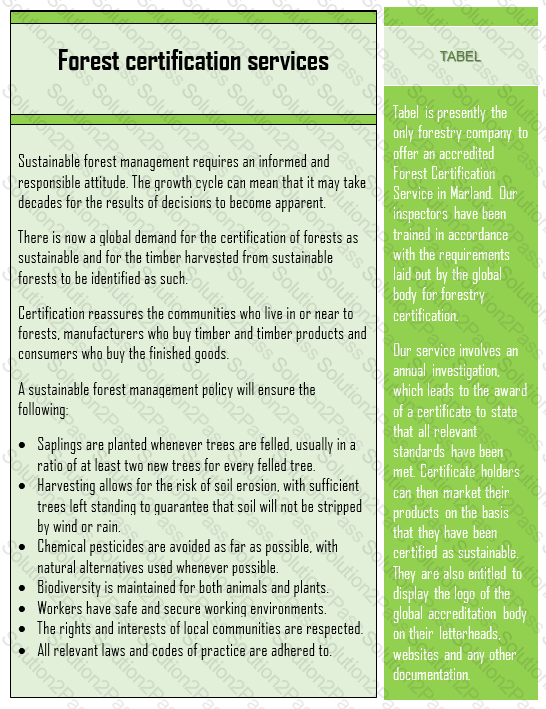

I have attached a sales brochure that I downloaded from Tabel’s website. Tabel is a competing forestry company that has similar interests to our own. It has recently launched the certification scheme that it has described in its brochure. It has no competition for this certification in Marland because no other company has sought the qualifications required to offer an accredited Forest Certification Service.

Wodd has the necessary skills to offer a credible Forest Certification Service. Our forestry managers already aim to exceed all of the requirements set out by the global body. We also have a well-resourced internal audit department. I believe that we could transfer either forestry managers or internal auditors to a new external certification department. The transferred staff would complete the training required by the global body and would sit the associated examinations. We could then compete with Tabel’s service.

I need your advice on the following:

Could you explain how you imagine that a typical certification investigation would work and the skills that it would require? That will help us to decide whether to approach forestry managers or internal auditors and will also enable us to describe the work that they would be doing if they agreed to be transferred.

What are the challenges associated with motivating and evaluating the investigators in the certification service and how might we address these?

Sarah

Reference Material:

A further eight weeks have passed since the discussion concerning Wodd’s creation of an accredited Forest Certification Service.

Wodd’s Chairman has asked you to a meeting:

"I thought that we had a lucky escape over the Barry Crauder story from a recent news article, but the Government is considering modifying the tax arrangements associated with forestry. Professional forestry companies such as Wodd will continue to pay no tax on forestry profits, but private individuals such as Mr Crauder will be taxed on profits just as they would for any other business. The Government is taking this action because public opinion is against granting generous tax relief to wealthy individuals.

For the moment, this is all highly secret. The minister responsible for forestry has spoken to the chairmen of all of the major forestry companies on the basis that each gives a personal guarantee to respect the Government’s confidence. The minister has done so because she is concerned that stock markets will panic when the news of the tax changes are announced next week. If the shareholders incorrectly believe that we will lose the tax shield on our profits then the share price will drop like a stone. We will be able to announce that we are aware of the changes and that we will not be taxed differently because of them.

I have spoken to the Board about this, making them promise not to repeat any of this information. We have called in and briefed the key analysts who advise the main institutional investors in Marland on the forestry industry.

As things stand, we can expect a lot of the wealthy individuals who own forests to divest themselves as soon as they discover that there are no more tax incentives. That will have significant implications for Wodd, both directly and indirectly.

The Board believes that the markets will overreact when the tax changes are first announced and that we will be unable to do much to manage that. One suggestion that has been put forward is that we should increase the dividend slightly as a signal that we are confident in the future strength of the industry. I suspect that the executive directors are just a little too concerned with the fact that they all have stock options that can only be exercised on a date that falls just after the government is due to announce its intentions on tax.

I need your thoughts in order to have an independent viewpoint from that voiced by the Board:

What effect will the tax changes have on our business?

Do you agree that briefing the analysts will mitigate the risk of our share price overreacting when the tax changes are announced?

Will the additional dividend payment help to maintain the share price?

Is granting executive stock options always a sound basis for aligning the interests of the executive directors and the shareholders?"

You have received the following email from Marcus Svenson, Finance Director:

From: Marcus Svenson, Finance Director

To: Senior Finance Manager

Subject: Investment opportunity

Hi,

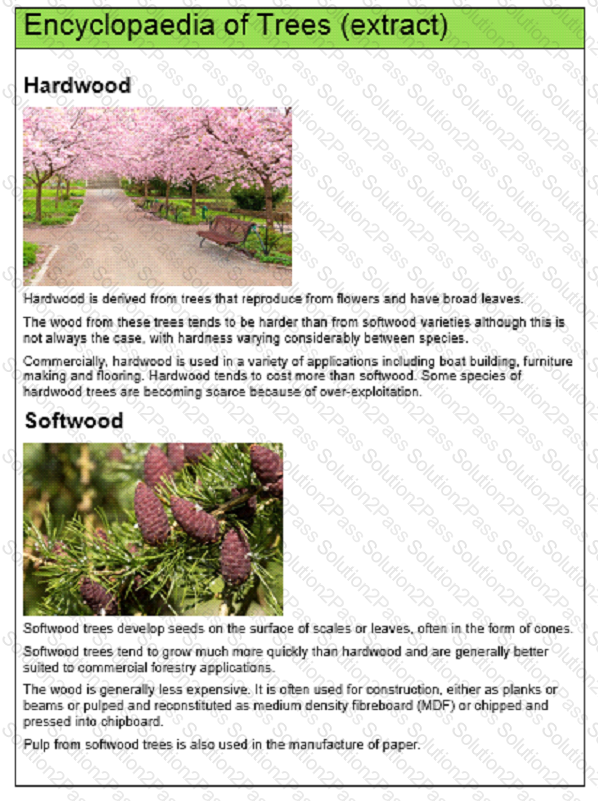

The Board is considering an investment opportunity to buy a forest in Bravador, a country in South America. This will be a major expansion and will also enable us to diversify into new lines. For example, the forest contains lots of hardwood varieties that we could sell to companies in the double glazing industry or to furniture manufacturers. I downloaded the attached extract from an online encyclopaedia for your information.

The forest that we are planning to buy has not been used for commercial purposes until now. The land belonged to the Government for many years and it has been left to grow naturally. The Government is now keen to sell the land and has agreed that it may be used for commercial forestry purposes.

This investment will enable us to increase our output of softwoods by up to 20% per year, in addition to enabling us to enter the hardwood market.

I need two things from you. I need you to recommend a suitable approach to managing our relationship with the Bravadorian Government. I also need you to identify and explain the political risks that will remain even if we succeed in creating a sound relationship with the Government.

Marcus

Reference Material:

A week later, Romuald Marek stops by your workspace and hands you a document.

The Board minute extract from Romuald can be viewed by clicking the Reference Material button above.

Reference Material

Board minutes extract: proposal to profit from ongoing strength of NS

Anna Obalowu Sole, Chief Operating Officer, reported that the strong NS was helping generate revenues from fuel sales. Discussion followed as to whether the strong N$ was likely to persist and whether a strong N$ benefits Arrfield overall.

Markus Jokela. Chief Executive Officer, stated that the Board should develop contingency plans that could be implemented if it seemed likely that the strong N$ would persist. In particular. Arrfield need not renew the contracts that permit aviation fuel suppliers to operate from its airports. Arrfield would then be free to create its own fuel sale business, buying fuel in bulk to replenish the storage tanks at each of its airports in Norland and then selling it directly to airlines He stated that this would almost certainly enhance Arrfield's share price

Romuald Marek reminded the Board that four of Arrfield's six airports are located in Norland and that those airports charge for aeronautical and non-aeronautical services in N$.

Hello

I have attached a news article

Arrfield does not set the price for aviation fuel sold at our airports, but we do receive a percentage of the revenues earned by the fuel companies.

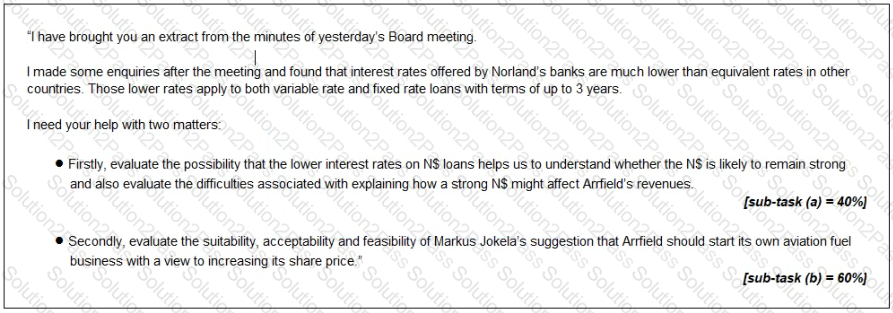

I need your help to prepare for a Board meeting to discuss this matter Please write a paper covering the following

* Firstly, explain the impact that the criticisms voiced by the environmental campaigners will have on the frequent PESTEL analysis that Arrfield's Board conducts.

[sub-task (a) = 34%

* Secondly, evaluate the commercial logic of Arrfield's strategy of basing charges for non-aeronautical services (such as fuel sales and retail activities) on percentages of the revenues generated by the companies that operate at its airports

[sub-task (b) = 33%)

* Thirdly, recommend with reasons whether Arrfield should attempt to justify strategic decisions to its shareholders when the commercial logic of those decisions is not immediately obvious

[sub-task (c) = 33%}

Thanks

Romuald Marek

Chief Finance Officer

A month later, you receive the following email:

Reference Material:

From: Hesham El-Sayed. Independent Non-executive

Director

To: Romuald Marek. Chief Finance Officer

Subject: Collapse of fuel supplier

Hi Romuald

I am writing to give you some advance notice of an internal audit investigation that has been commissioned by the Audit Committee

Just over a year ago. Planejoos, a newly formed company, approached the management team at Airfield's Capital City International (CCI) airport and offered to take over refueling operations at Starport Planejoos offered a higher percentage of revenue than the existing supplier was paying CCI's management team agreed and appointed Planejoos rather than renew the existing supplier's contract.

CCI was unable to conduct the usual background and credit checks on Planejoos for two reasons. Firstly, Planejoos was a new company and so did not have an extensive credit history that could be checked Secondly CCI was under time pressure to reach a decision on whether to renew the existing supplier's contract or allow it to expire

CCI's management team claimed that it had acted quickly in order to benefit from the additional revenue that could be earned from dealing with Planejoos The management team was acting on the basis that it had an ethical duty to maximise the wealth of Airfield's shareholders and that maximising revenues from fuel sales through this agreement with Planejoos was consistent with that ethical duty.

Unfortunately, as a new company. Planejoos struggled to obtain trade credit and the high demand for fuel put the company's cash flows under extreme pressure Receipts from sales lagged behind payments for inventory Planejoos has now collapsed, leaving a large trade receivable that CCI will have to write off as uncollectable CCI had permitted this receivable to accumulate rather

than pressing for payment and so putting Planejoos under further pressure.

Fortunately, the previous fuel supplier was prepared to return to CCI.

Kind regards