IIA-CIA-Part2 IIA Internal Audit Engagement Free Practice Exam Questions (2026 Updated)

Prepare effectively for your IIA IIA-CIA-Part2 Internal Audit Engagement certification with our extensive collection of free, high-quality practice questions. Each question is designed to mirror the actual exam format and objectives, complete with comprehensive answers and detailed explanations. Our materials are regularly updated for 2026, ensuring you have the most current resources to build confidence and succeed on your first attempt.

A bakery chain has a statistical model that can be used to predict daily sales at individual stores based on a direct relationship to the cost of ingredients used and an inverse relationship to rainy days. What conditions would an auditor look for as an indicator of employee theft of food from a specific store?

An internal auditor develops an engagement observation related to an organization ' s accumulation of large travel advances. The auditor observes that the organization ' s procedures do not require justification for travel advances greater than a specific amount Which of the following best describes the organization ' s procedures?

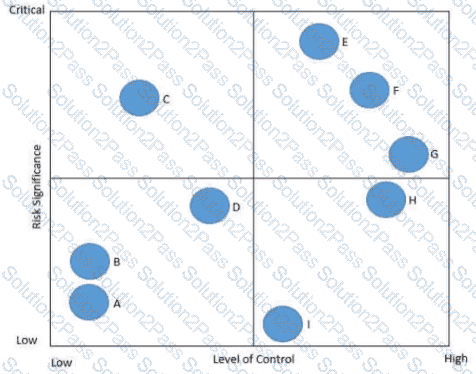

In the following risk control map risks have been categorized based on the level of significance and the associated level of control. Which of the following statements is true regarding Risk C?

An internal auditor using the five-attribute approach to document deficiencies in a warehouse shipping process. Which of the following attributes will be included in the workpapers?

According to IIA guidance, which of the following is a limitation of a heat map?

Which of the following internal control attributes should internal auditors consider testing during a review of the board of directors?

A chief audit executive (CAE) following up on action plans from previously completed audits identifies that management has determined that certain action plans are no longer necessary If the CAE disagrees with managements decision, which of the following is the most appropriate next step for the CAE to take?

A chief audit executive (CAE) reviews the supervision of an internal audit engagement Which of the following would most likely assure the CAE that the engagement had adequate supervision?

During the preliminary survey of the procurement department, an internal auditor noted a major control weakness in the organization ' s ordering and receiving process. According to IIA guidance, which of the following is the most appropriate action the internal auditor should take?

An internal auditor is planning an engagement at a financial institution. Toe engagement objective is to identify whether loans were granted in accordance with the organization ' s policies. When of the following approaches would provide the auditor with the best information?

According to IIA guidance, which of the following statements is true regarding engagement planning?

An internal auditor at a bank informed the branch manager of a malfunctioning lock on one of the vaults. The risk associated with this issue was deemed significant by the chief audit executive (CAE), and immediate remediation was recommended. However, during a follow-up engagement, the branch manager told the CAE that the risk was actually not significant, hence no action was taken. What is the most appropriate next step for the CAE?

Which of the following should an internal auditor document to support an assurance engagement’s conclusions?

Which of the following is the next step in understanding a business process once an internal auditor has identified the process?